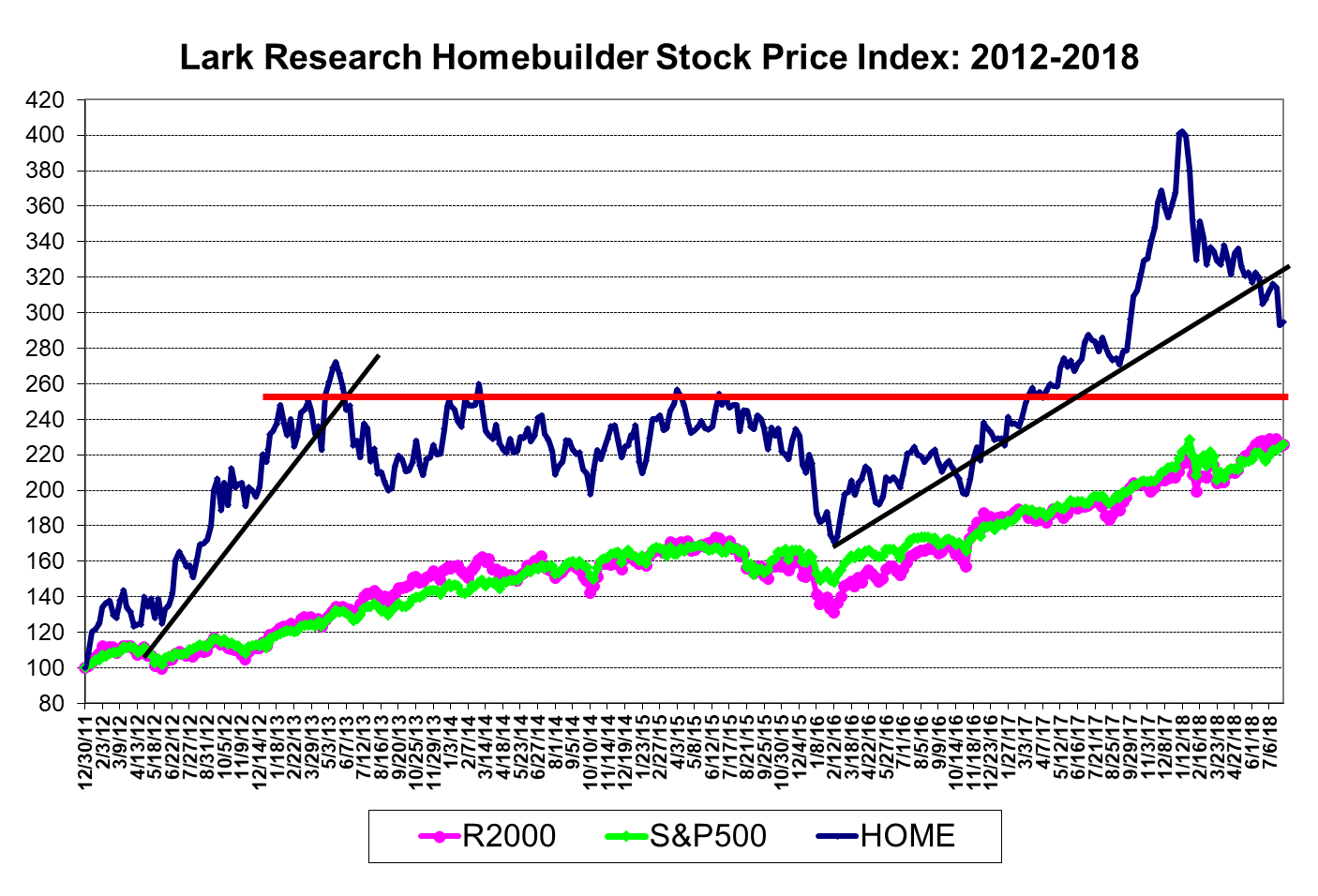

2018 has been rough for homebuilding stocks. The Lark Research Homebuilder Stock Index, which is an equal-weighted measure of the price performance of ten publicly-traded homebuilders, was down 19.9% year-to-date through August 3rd, far worse than the gains of 6.2% in the S&P 500 and 9.0% in the Russell 2000.

This year’s decline, while noteworthy, requires a more complete explanation: Fueled perhaps by the euphoria surrounding the passage of the Tax Cut and Jobs Act, which may have driven double-digit increases in new orders, homebuilding stocks went parabolic at the end of 2017, rising 48% during the fourth quarter. They then fell nearly 18% on average over the first five weeks the new year. Since then, the homebuilders have been grinding steadily lower, but the pace of the decline seems to have picked up some in recent weeks.

The Big Picture. This speculative boom and bust in homebuilding stocks is similar to the pattern of the 2005 peak, which culminated three years later in the collapse of the housing and financial markets. Back then, the housing market was clearly overheated, fueled by above-trend economic growth, rapid house price appreciation and lax mortgage underwriting standards. A steady rise in the default rate on mortgages, especially subprime mortgages, gathered steam in 2007.

Today’s technical setup for homebuilding stocks is worrisome. The chart suggests that the sector is still searching to find bottom. Weakness in homebuilding stocks undoubtedly reflects concerns about rising mortgage rates and perhaps a coming slowdown in global economic activity due to rising trade tensions. Given the similarity to the pre-financial crisis bust, this year’s price spike and subsequent sell-off demands vigilance.

Yet, there are some notable differences today. This time around, there are few signs of speculative excess. Perhaps the most ominous sign is the unrelenting climb of house prices at a 6.5% average annual rate since 2011, according to Case-Shiller. This extended advance is due to the combination of historically low interest rates and limited supply of for-sale inventory. At its most recent reading (May 2018), Case-Shiller’s national house price index was nearly 10% above its July 2006 peak.

The pace of acceleration in house prices has clearly exceeded the average annual increases in both inflation and wages. Inflation, as measured by the CPI, has averaged 1.6% annually since 2011. Average weekly earnings have risen at a 2.4% annual rate over the same period. Growth in household income picked up in 2015 and 2016 (the last year of data from the Census Bureau), averaging nearly 5% in each of those years; but that is still below the rate of house price appreciation. With the rapid rise in house prices, housing has clearly become less affordable since the financial crisis.

Still, a speculative blow-off in housing is nowhere in sight. Single-family housing production remains at roughly half the 2005 peak. Single-family starts and permits have been running at about 850,000 annual units so far this year, half of the 2005 peak of 1.7 million units. New home sales have totaled 636,000 units over the latest 12 months, also equal to half the 2005 peak of 1.28 million units.

At the same time, tighter mortgage underwriting standards have kept the mortgage market in relatively good shape. For example, the percentage of mortgages entering default fell to just 0.63% in June, according to the S&P/Experian First Mortgage Default Index. That is the lowest level recorded since the Index was created in July 2004. (Similarly, the S&P/Experian Composite Consumer Credit Default Index, which measures new defaults in first and second mortgages, credit cards and auto loans, also fell to a record low in June.)

With few traditional signs of a speculative bubble, still modest housing production levels and low mortgage default rates, an imminent collapse of the housing market seems highly unlikely.

The housing market could conceivably suffer a major setback in response to a sharp decline in economic activity. Given recent trends and consensus forecasts of continuing economic growth, however, such a collapse would probably have to sparked by a so-called “black swan” event such as a major terrorist attack or an outbreak of war.

Recent Housing Market Trends. Since the parabolic spike, the continuing decline in homebuilder shares is probably due to the leveling off of new home sales in recent months (and the recent decline in existing sales). With the anticipation of more rate hikes to come from the Fed, higher mortgage rates could further slow housing activity.

According to the most recent Commerce Dept. report, new home sales started the year with solid gains; even though the year-over-year percentage increases were more moderate than in prior years. Estimates of new home sales made in January were revised upward, but as the Spring season wore on, the revisions turned negative and the pace of sales slowed. June’s estimate of a 631,000 unit seasonally-adjusted pace, which is still subject to revision, was up only 2.4% from a year ago. Year-to-date, the Commerce Dept.’s estimate of actual sales is still up 7.4%, but that is still slower than last year’s 11.6% increase for the comparable period. Investors are apparently concerned that the recent pattern of downward revisions and decline in June new home sales signals more slowing in the months ahead.

The National Association of Realtors (NAR) recently reported that the annualized pace of existing home sales declined for the third consecutive month in June to a rate of 4.76 million units. June’s pace was down 0.6% from May and 2.3% from the prior year. The NAR asserted that the decline is due to a mismatch between strong and rising demand and the limited number of homes available for sale. It claims that houses that are listed are selling quickly; but there is not enough supply in many areas. Yet, by its own estimates, the number of homes in inventory nationwide increased 35% to 1.74 million from December to June, while the months’ supply of inventory rose to 4.4 months, from a low of 3.1 months in December. That measure of inventory to sales is consistent with longer-term (pre-financial crisis) averages.

The NAR data also show that most of the decline in existing home sales in recent months has been concentrated in the lower price points. Sales of more expensive existing homes are still on the rise. The drop in lower-priced home sales is consistent with the view that the combination of higher home prices and rising mortgage rates is at the very least causing some potential buyers to postpone their purchase decisions.

Despite the concerns about a lack of existing home inventory, the supply of new home inventories available for sale remains at an acceptable level, between five and six months’ worth of sales over the past five years. The data suggests that the homebuilding industry is not saddled with excess inventory that might have to be discounted in the event of a decline in new home sales.

Homebuilder Operating Performance. Although 2018 second quarter new order growth slowed, builders remain upbeat about their prospects for the balance of the year and beyond. The average builder, according to my calculation and estimates, posted growth in new unit orders of 5.8% in the quarter. That was up slightly from the 5.4% recorded in the 2017 second quarter, but down from the low double-digit gains recorded in the 2017 fourth quarter and 2018 first quarter.

Some details about my calculations are in order: First, the change in reported homebuilder net orders is a simple average of the percent change in orders reported by eleven publicly-traded builders (BZH, DHI, HOV, KBH, LEN, MDC, MHO, MTH, NVR, PHM and TOL). The average reported for the 2018 second quarter does not include HOV and TOL, which have yet to report results. In addition, in this latest quarter, I have adjusted the percent change reported by Lennar from 48.9% to 11.3%. Lennar’s results for the quarter were skewed by its recent acquisition of CalAtlantic Homes. My adjusted 11.3% gain adds together the 2017 second quarter orders posted by Lennar and CalAtlantic. (This is not an accurate measure since these builders did not have the same quarter ending date; but I believe it does provide a better estimate than Lennar’s as-reported net order growth.)

With those caveats, my figures suggest that the rate of growth in new orders did slow in the 2018 second quarter from the immediately preceding quarters to a rate that is more consistent with the prior year. Of course, the market is worried that order growth will slow further in the 2018 third quarter, so we will have to wait until those results are released in mid- to late-October to confirm or nullify that fear.

Management commentary on the 2018 second quarter earnings conference calls also provides some potential insight into the future course of homebuilder operating and financial performance. It is fair to say that the comments were mixed. A few builders acknowledged both the recent slowdown in their orders and said that they were watching buyer traffic and order trends closely; while others reported little or no impact from the recent increase in mortgage rates. Three builders (BZH, MDC and PHM) reported that orders slowed in May as mortgage rates were on the rise, but then picked up again in June. Pulte said that traffic was strong in May, but the percentage of traffic converted to contracts declined. KBH said that its relatively modest 3.4% increase in net orders was due to a temporary decline in its community count, offset partially by an increase in sales per community.

Despite the slowing in new order growth, all of the builders remain upbeat about the outlook for their businesses, primarily because of the positive macro environment (e.g. strong job growth, low unemployment, increasing wages, high consumer confidence and until recently a limited supply of existing home inventory). Nearly all still characterize most of their markets as robust or solid. They are seeing strong traffic from millennials, who are now in their peak home buying years. They do acknowledge, however, that affordability is an issue. So far, the builders say that they have been able to pass on increases in labor and materials costs (e.g. lumber and steel), but rising mortgage rates will likely limit their ability to raise prices to cover these costs.

While sellers of existing homes are limited primarily to one tactic in the face of rising mortgage rates – adjusting price – builders have at least several ways to alter their strategies. Over the past few years, many of the publicly-traded builders have increased their offerings of lower-priced homes for entry level (and move-down) buyers, which represents the market segment with the greatest potential for growth. Although this segment is also quite sensitive to changes in mortgage rates, builders can over time adjust the prices that they pay for land, where they buy land, their home designs and purchase options and amenities offerings. While profit growth may lag during this adjustment process, most builders should be able to adjust successfully, as long as the increases in mortgage rates are gradual. Since the Fed has been telegraphing its plan to normalize interest rates for several years now, I would expect that most builders incorporated potential mortgage rate increases into their land purchase decisions some time ago.

The Process of Adjustment. After this year’s declines, the average homebuilder (of the eleven that I follow) now trades at 9.0 times anticipated 2018 consensus earnings and 8.0 times projected 2019 earnings. The 2018 earnings projections expect average earnings growth of nearly 60% from GAAP 2017 earnings, according to my calculation. 2019 consensus projections predict average earnings growth of about 15%.

Based upon the average earnings beats for the first two quarters, I estimate that 2018 consensus earnings have increased about 8% since the beginning of the year. Along with the 20% decline in the average homebuilder share price, that implies that the 2018 earnings multiple for the homebuilders has fallen from about 12 at the beginning of the year to 9 currently.

One key determinant of future homebuilder share performance will be whether the 2019 consensus estimate holds up in the face of rising mortgage rates. That, in turn, will be driven by the actual and expected course of mortgage rates over the next six months.

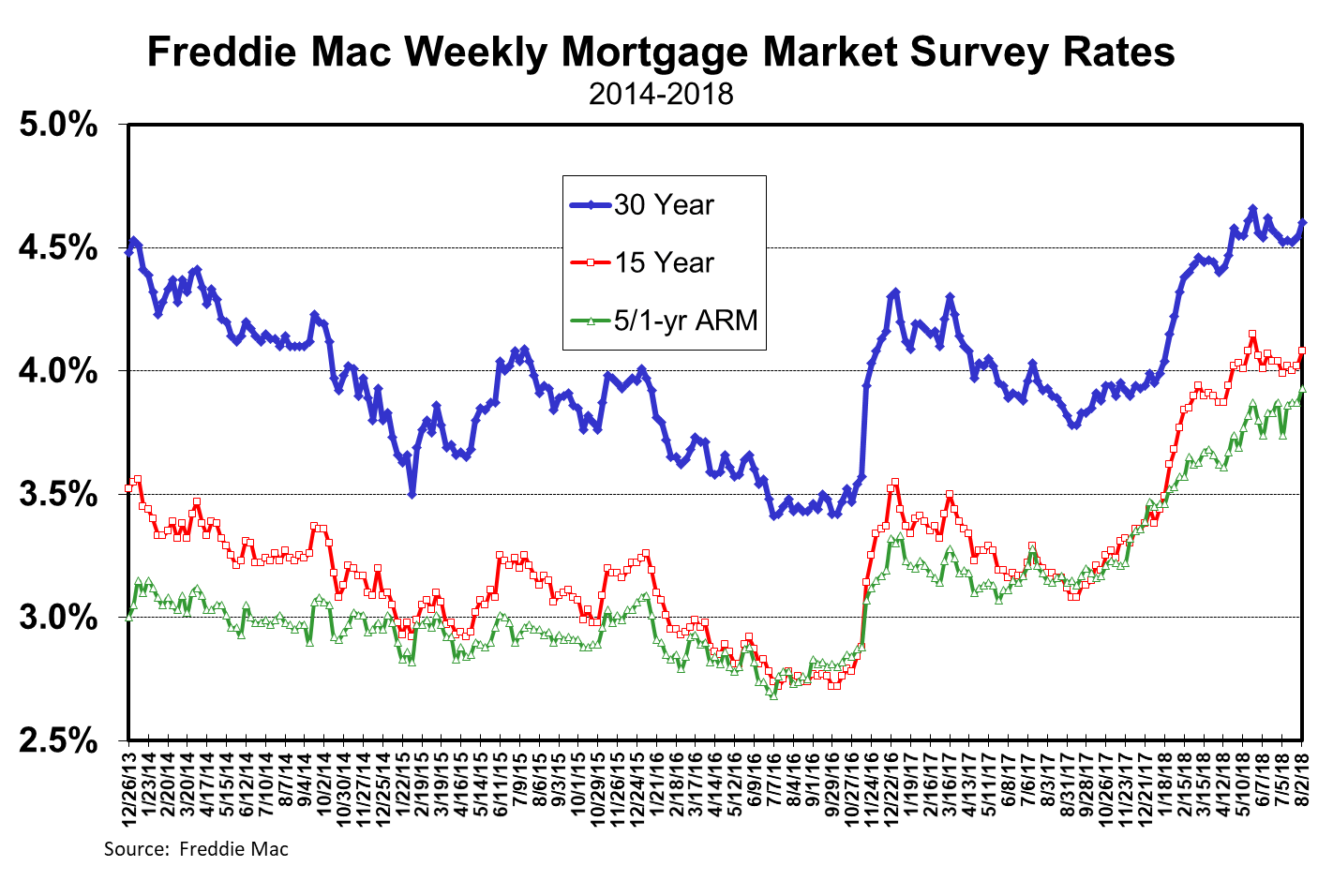

As of today (8/9), the average rate on a 30-year mortgage was 4.59%, according to Freddie Mac. That rate has fluctuated between 4.52% and 4.66% since mid-May. If the yield on the 10-year Treasury remains at around 3.00%, I expect that the 30-year mortgage rate will eventually drift up to 4.75%, especially if the FOMC raises the target Fed Funds range by another 25 basis points (to a range of 2.00%-2.25%) at its next meeting in September. After that, futures currently assign a 64% probability that the Fed Funds target range will rise another 25 basis points by the FOMC’s December meeting. If so, the 30-year mortgage rate could approach 5.00% by then.

To put this in perspective. Another 50-basis point increase in the 30-year mortgage rate would raise the monthly payment (including mortgage, property taxes, house insurance and mortgage insurance for those who put down less than a 20% downpayment) by about 4%. At the median price for new homes of around $300,000. This would also raise the annual income required to purchase that house by 4% from $79,200 to $82,400.

Coming on top of a 60-basis point increase in mortgage rates since the beginning of the year, which has already raised monthly payment and income requirements by about 5%, buyers may have to come up with as much as 9% more income by the end of the year to afford that same house that they were eyeing at the beginning of the year.

Given the slowdown that we have seen in existing home sales and new orders in recent months, it is clear that the 5% rise in income requirements has already had some impact, especially among marginally qualified buyers. While there may be an initial “deer in the headlights” response among buyers as rates are on the rise, as they were last May, eventually buyers who really want to buy will recognize that they and perhaps the sellers will have to make some adjustments in order to complete the sales transaction.

Obviously, there are lots of ways to adjust. Buyers can opt for a lower-priced house, find a way to make a bigger downpayment or wait for their next pay increases. Sellers can reduce prices. Builders can sell a less expensive floor plan or one with fewer add-ons. Over time, builders can make more extensive adjustments to their subdivisions. Still, assuming that economic conditions remain favorable, investors should see this as a process of adjustment rather than an impending downturn in the housing industry.

Accordingly, this year’s decline in homebuilder share prices, admittedly from what now clearly look like unsustainably high prices at the beginning year, should be recognized as a process of adjustment for the housing market. Given buyer income constraints, it is virtually certain that builders will have to shoulder some part of the recent and anticipated increases in mortgage rates. They almost certainly will not be able to raise prices as fast as they were over the past several years. They also may see some erosion in operating margins.

With the increases in sale and profits already booked to date and still expected in the second half, builders have posted revenue growth in the mid-teens and operating margin expansion averaging about 150 basis points to 8.5% on average, according to my calculations. Unless buyers are able to adjust completely (after the second quarter pause) to what will likely be a 100-basis point increase in mortgage rates, It is probable that 2019 revenues will grow at a slower rate, perhaps in the low-to-mid-single digits and operating margins decline some from 2018 elevated levels.

The combination of the two – slower revenue growth and lower operating margins – may make it difficult for builders to achieve growth in earnings (and earnings per share) in 2019. But it is also fair to say, as long as economic growth remains solid, that the builders will make adjustments in the 2018 second half and into 2019 that should put them back on a growth path in 2020. Thus, their share prices should also complete the process of adjustment, bottoming sometime in the second half and establishing a base from which they can mount an advance sometime in 2019.

That bottom will undoubtedly be influenced by the outlook for further interest rate normalization in 2019. Many economists anticipate another three or four 25-basis point rate hikes in 2019. If so, that could bring the 30-year mortgage rate to 6.00% by the end of the year and raise the income requirement for the same dollar equivalent mortgage amount by a total of 17% from the beginning of 2018. In my view, that would deal a crushing blow to the housing market, causing major declines in both existing and new home sales. That is one reason why I think that it is likely that the FOMC will pause by the end of 2018 or early in 2019.

The stock market undoubtedly has all of this figured out and so will be looking to see how the Fed will proceed on raising rates as the year comes to a close. If the FOMC continues to signal more rate hikes to come, homebuilding stocks will probably continue to struggle to find a bottom. At present levels, the sector already looks cheap compared to its earnings potential over the next few years (assuming a reasonable and pragmatic FOMC), so the end of the rate hikes could be a catalyst for recovery in the sector.

August 9, 2018

Stephen P. Percoco

Lark Research

839 Dewitt Street

Linden, New Jersey 07036

(908) 448-2246

admin@larkresearch.com

© Lark Research, Inc. All rights reserved. Reproduction without permission is prohibited.

Discover more from Lark Research

Subscribe to get the latest posts sent to your email.