Since it was spun off from Hewlett-Packard Company in November 2015, Hewlett Packard Enterprise Company (HPE) has made several important strategic moves to remake its business.

On April 1, 2017, HPE completed the spin-off of its Enterprise Services business (known as “Everett”) and Everett subsequently merged with Computer Sciences Corporation. The new company is called DXC Technology Company (DXC). HPE shareholders received 0.085904 shares of DXC for each share of HPE. That represented a 50.1% equity stake in DXC, which HPE valued at $4.5 billion. HPE also received a $1.5 billion cash dividend and DXC assumed $2.5 billion of HPE debt. From the first day of trading, DXC shares were priced at more than twice their initially estimated value. They have since risen 22%. Based upon DXC’s current value, the spin-off was worth $7.16 per HPE share.

On September 9, 2016, HPE announced a planned spin-off and merger of its Software segment (a/k/a “Seattle”) with Micro Focus International PLC (MFI). Based in the UK, Micro Focus, which trades under the ticker symbol MCRO.L, is a roll-up of mature software companies that offer long established products, such as COBOL, mainframe software, identity, access & security (IAS) products, collaboration & networking solutions, and relatively newer offerings, such as open source software. While MFI aims to keep its mature product offerings relevant to its installed base, it is also looking to expand its capabilities in newer areas. For example, It has announced plans to offer two cloud-based services – Platform-as-a- Service (PaaS) and a Container-as-a-Service (CaaSP) – which provide cloud infrastructure on demand so that users can develop cloud-based applications quickly and at a significantly lower costs. Since 2005, MFI has completed 15 acquisitions, including Attachmate Group in 2014, itself a roll-up that owned Novell, a pioneer in networking and identity software, and SUSE Linux, a leader in open source software. In March 2017, SUSE acquired certain assets and employees related to HPE’s Helion OpenStack and Stackato businesses. In return, HPE named SUSE its preferred open source partner for Linux, OpenStack and Cloud Foundry solutions.

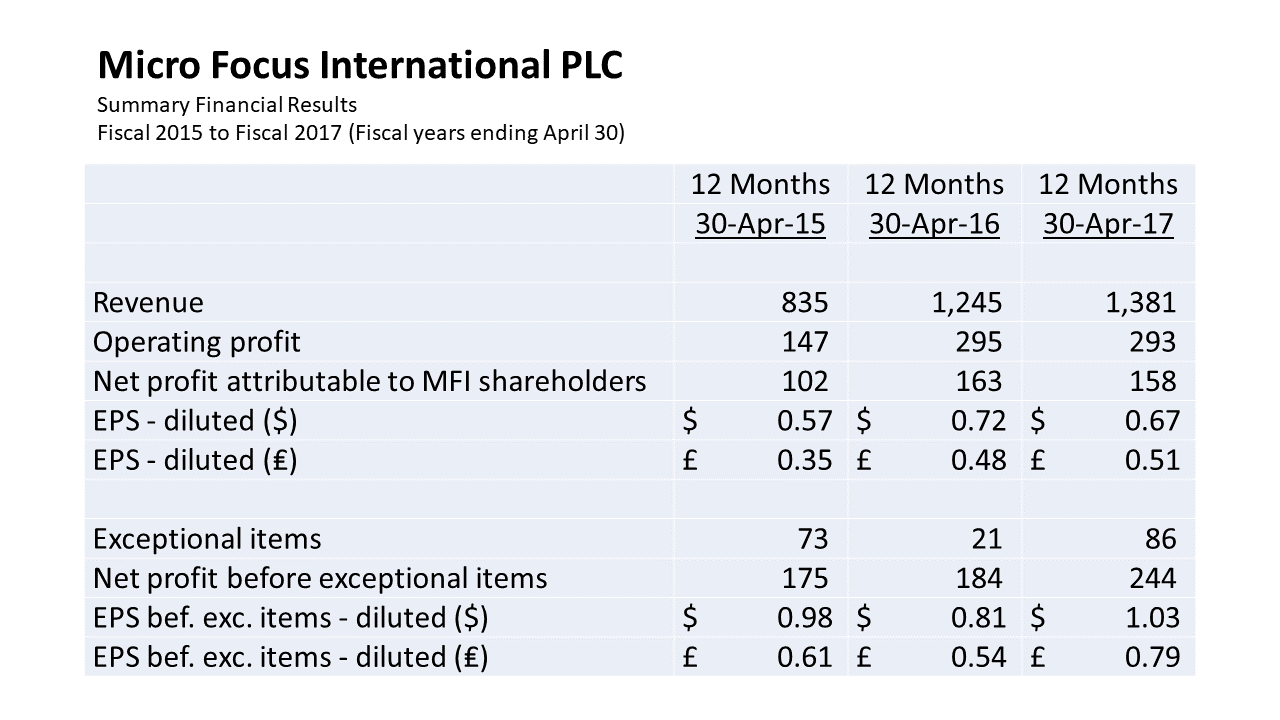

MFI’s revenues have increased 65% over the past two fiscal years; its operating profit has doubled and its net profit is up 55%. As a roll-up, the company regularly incurs costs to acquire and integrate target companies. In the financial statements included in the merger prospectus, MFI refers to these costs as exceptional, suggesting that they are unusual in nature and investors might consider excluding such costs to get a better picture of MFI’s future performance (once it stops acquiring and integrating companies). As shown in the chart above, MFI’s EPS under international financial reporting standards (IFRS) was equivalent to $0.67 per share in fiscal 2017 (ended April 30). Excluding exceptional items, its adjusted EPS was $1.03.

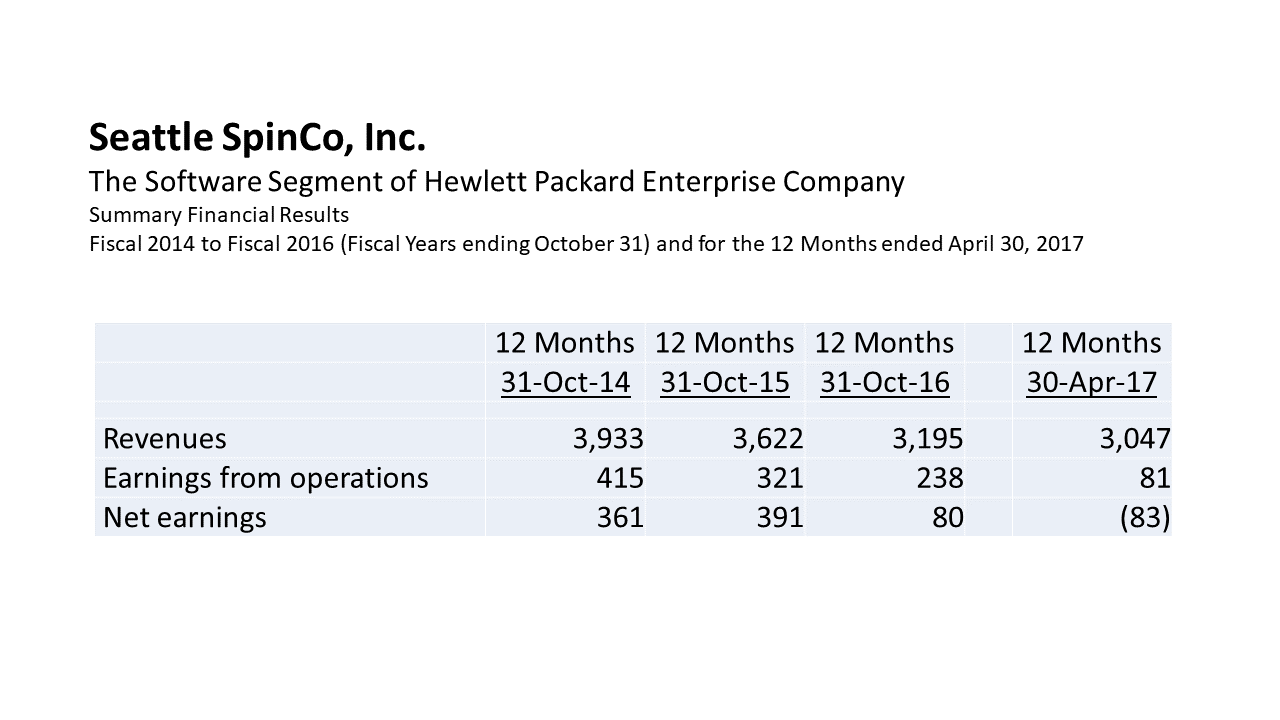

HPE’s Seattle software segment offers big data platform analytics, application & delivery management software, security & information governance solutions and IT operations management software. Accordingly, it will allow MFI to expand its presence in several of its established product areas and also enter the business of big data analytics. The acquisition is a good strategic fit. However, Seattle has been struggling in recent years and its financial performance has been deteriorating. Over the past two-and-a half years, Seattle’s revenues have fallen from $3.9 billion to a run rate of $3.0 billion; while GAAP net earnings have fallen from $360 million to a loss of $83 million.

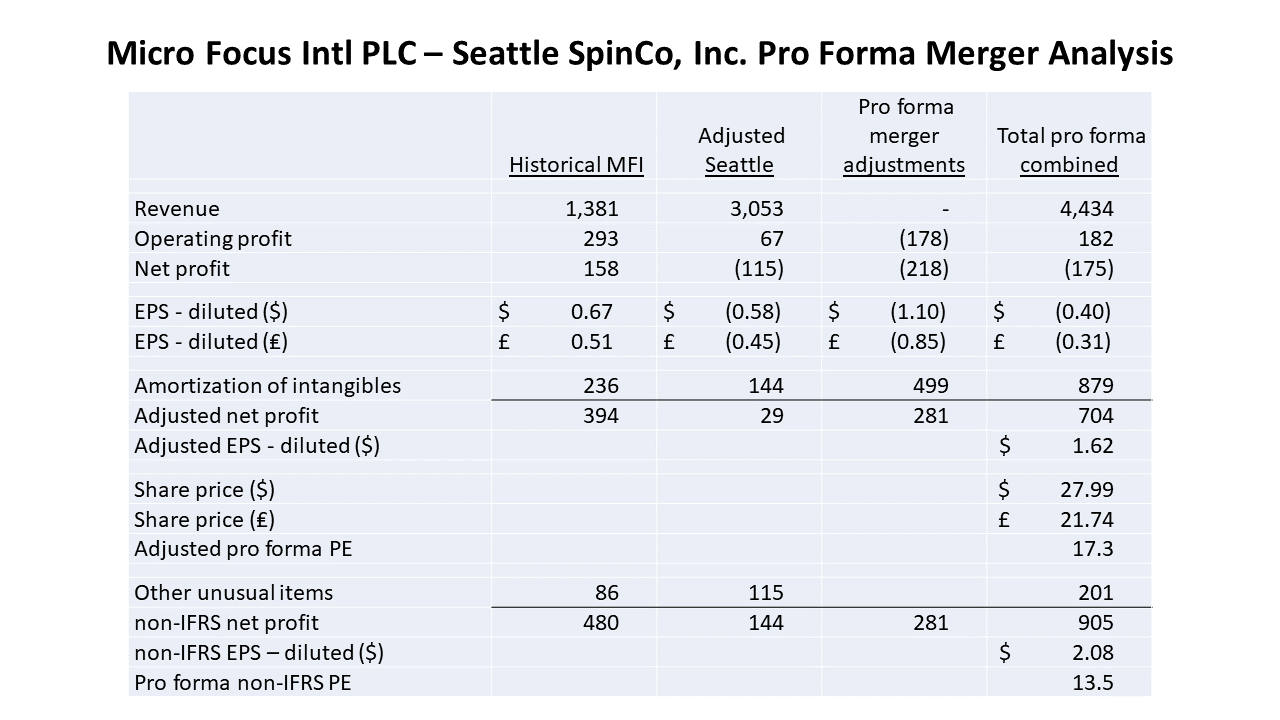

The acquisition will more than triple MFI’s revenues on a pro forma basis (for the fiscal year ended April 30, 2017) from $1.38 billion to $4.43 billion, but it would reduce MFI’s fiscal 2017 earnings from a profit of $150 million to a deficit of $175 million. (On a pro forma per diluted share basis, MFI’s reported fiscal 2017 EPS falls from $0.67 per share to a loss of $0.40 per share.

The pro forma analysis, as shown in summary form in the table above, illustrates the impact of the merger on MFI’s fiscal 2017 results. In the second column, it adds in Seattle’s financial results for the 12 months ended April 30, 2017, adjusted to IFRS standards. Those IFRS adjustments increase Seattle’s reported net loss from $83 million to $115 million. Seattle’s $115 million net loss reduces MFI’s pro forma EPS by $0.58. The third column contains three adjustments associated with the merger: (1) a $499 million increase in intangibles amortization costs (as a result of writing up intangible assets by $6.5 billion); (2) a $148 million increase in interest expense due to an anticipated $3.3 billion increase in debt and (3) a reduction in operating costs of $321 million to eliminate expenses that were incurred by MFI and Seattle during the year that are not relevant to the merger. This includes $276 million to back out costs incurred by Seattle to separate its operations from HPE and $45 million of merger costs incurred by MFI (that are not expected to have a continuing impact on MFI after the closing). In total, the net adjustments in the third column reduce pro forma EPS by $1.10 per share.

Amortization of intangibles is a non-cash expense that is typically excluded from earnings, as a non-GAAP adjustment. For acquisition-oriented companies like MFI, the purchase price of software companies usually exceeds the fair value of their tangible assets. The difference is allocated first to intangible assets, like patents, customer relationships and trade names, and then to goodwill. Intangible assets are typically amortized over 10 years (20 years for trade names). Because its annual intangible amortization charges are high, MFI usually generates more cash flow from operating activities (CFOA) than net income. For example, in fiscal 2017, MFI reported net income of $157.8 million and CFOA of $452.4 million. In fiscal 2016, its net income was $163 million and CFOA was $283.2 million. In fiscal 2014, MFI’s net income was $101.5 million and its CFOA was $200.3 million. Thus, many analysts exclude intangible asset amortization from GAAP earnings to create a non-GAAP EPS measure that is more closely aligned with the cash flow generating capability of the company.

In total, including the $499 million in annual amortization from the write-up of intangible assets, I estimate that MFI has total intangibles amortization costs of $879 million on a pro forma basis (as shown in the table above). Adding these costs back to net earnings raises MFI’s pro forma EPS from a $0.40 loss to a $1.62 profit.

In addition, there are other unusual items that are often added back in a non-GAAP reconciliation – namely the $85 million of exceptional items, recorded by MFI in fiscal 2017 (as discussed above) and another $115 million of restructuring costs, acquisition costs and pension plan remeasurement benefits, net of tax. Together, these increase pro forma non-IFRS EPS by another $0.46, bringing the total to $2.08. Using that as a benchmark, MFI’s stock has a pro forma price-to-non-IFRS earnings multiple of 13.4.

It is best to approach non-GAAP earnings with caution and some skepticism. While most companies routinely have exceptional, unusual and one-time costs that may mask their underlying earnings potential, it is often the case that these exceptional costs show up every year. Acquisition-oriented companies like MFI routinely incur acquisition and integration costs, so these expenses should be viewed as recurring. It may be useful to consider what the company’s performance might look like once it stops making acquisitions, but that time may be many years away.

I usually view GAAP earnings as a better measure of a company’s historical performance and non-GAAP earnings as an indicator of a company’s potential future performance. However, there are certain non-GAAP adjustments – amortization of intangible assets is one; amortization of purchase accounting adjustments for inventory is another – that I think are usually appropriate as an adjustment to historical results. Otherwise, I prefer to consider each non-GAAP adjustment on a case-by-case basis.

In MFI’s case, I prefer my pro forma adjusted EPS figure of $1.62, which includes intangible amortization costs and Seattle’s separation costs, to the IFRS pro forma EPS of negative $0.40 to reflect MFI’s ability to generate cash flow.

Using the $1.62 figure, MFI’s price-to-adjusted pro forma earnings multiple is 17.2, which seems high right now; but there is an obvious opportunity for MFI to integrate its operations with Seattle’s, reduce operating costs and use its greater scale to win more business. Seattle is clearly a turnaround opportunity.

Using the $2.08 non-IFRS pro forma EPS estimate, which incorporates restructuring and related costs, MFI’s price-to-potential future earnings multiple is 13.5. Thus, if MFI can achieve stable performance at fiscal 2017 levels and eliminate exceptional or unusual expenses in the near future (say a year or maybe two), investors will have bought its shares today at a bargain price.

MFI plans to change its fiscal year end from April 30 to October 31 to align its fiscal year end with Seattle’s. There is a good chance that it will incur significant integration and restructuring costs after completing the acquisition.

MFI is one of the few software firms to offer a meaningful dividend. It plans to continue to pay its dividend at the current rate of ₤0.65 ($0.84), which equates to a 3.0% dividend yield at the current price of ₤21.74 ($27.99), even though its share count will double. At my lower pro forma adjusted EPS estimate of $1.62, the stock’s pro forma PE multiple of 17.3 is below its peer group’s average forward PE multiple of about 23 times anticipated 2017 earnings. Assuming a successful turnaround, investors are getting MFI at a discount and they are being paid adequately to wait for the company to deliver on its future earnings potential. I do not know how easy it will be to turn Seattle’s performance around. Part of the solution almost certainly involves right-sizing the cost structure, but stemming the revenue decline will probably be harder, given tough competition and a maturing industry.

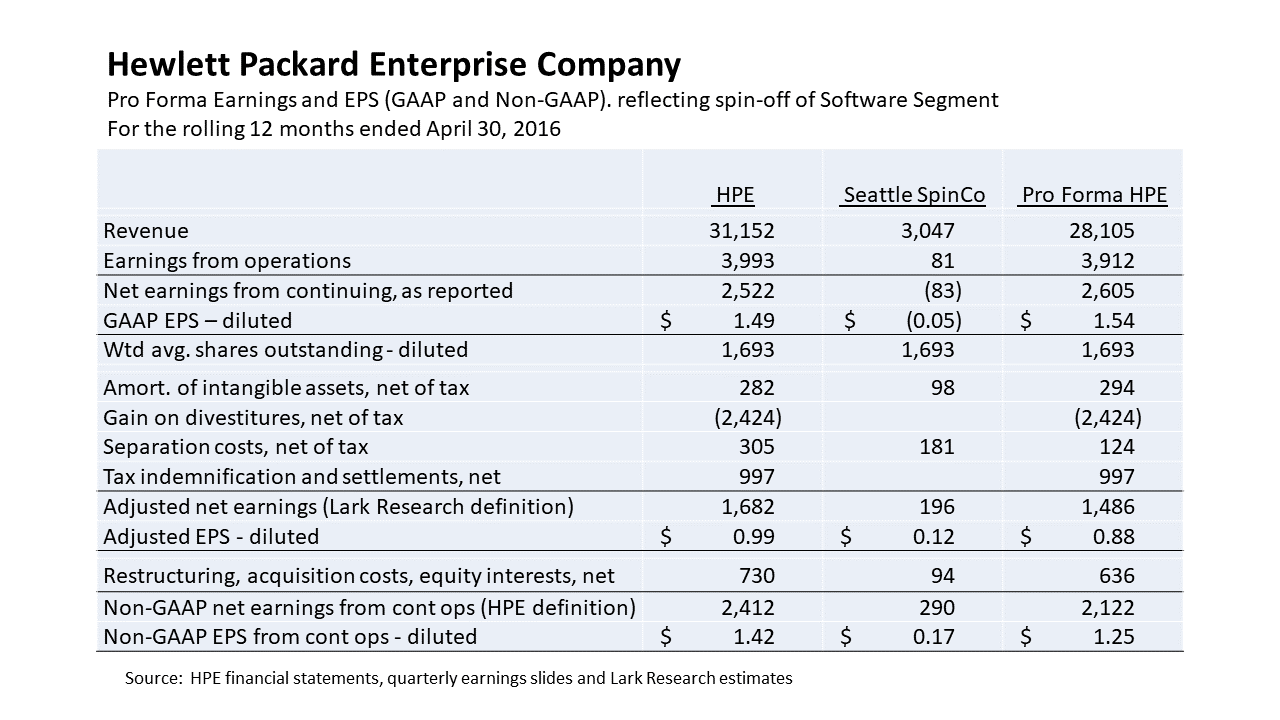

Although HPE will see its non-GAAP (i.e. potential) earnings decline slightly, the spin-off is positive for HPE and its shareholders. According to my calculations and estimates, as given in the table above, HPE’s pro forma rolling 12 months GAAP earnings will increase by $0.05 per share to $1.35 as a result of the spin-off, but its non-GAAP earnings (according to the company’s definition) will decline by $0.17 per share to $1.71.

Factors other than the EPS impact are also important. The spin-off allows HPE to focus management’s time and effort exclusively on its core Enterprise Group, where revenues and earnings have also been declining in a tough competitive environment. HPE will also receive $2.5 billion of cash, which increases its cash position as of April 30 to $10.6 billion on a pro forma basis. That compares with $13.9 billion of debt outstanding. The spin-off thus strengthens HPE’s financial condition, giving it greater flexibility to make additional acquisitions and investments or respond to adverse changes in its operating environment.

HPE continues to pursue its three core strategic pillars: (1) hybrid IT (i.e. the combination of data centers and cloud); (2) the intelligent (network) edge (which facilitates industrial IoT); and (3) services. Together, these markets are currently growing at only a low single-digit rate (with the intelligent edge growing in the mid-single digits). However, there are niches within these segments, such as flash memory, high performance computing, hyper-converged infrastructure (combining hardware and software-as-a-service (SaaS)), advanced network security and IT consumption analytics, that are growing at faster rates. In these niches, HPE is either accelerating the internal development of its product and service offerings or making acquisitions to gain access to technology and market share quickly.

HPE’s stock trades at a discount to its peer group. On a pro forma rolling 12 month basis, using my definition of non-GAAP EPS from continuing operations of $0.88 per share, its PE multiple is 19.5 times. Using the company’s non-GAAP definition, has EPS from continuing operations of $1.25 and a PE multiple of 13.7 times. Peers are currently valued at more than 25 times projected 2017 earnings.

HPE should not be incurring any more separation costs. Similarly, its restructuring costs should also be declining after nearly three years of remaking its business. The company may very well continue to incur costs related to future acquisitions, however, including restructuring and integration costs; but those should be lower than what it has recorded over the past three fiscal years. Accordingly, HPE’s definition of non-GAAP earnings may be a better indicator of its medium-term performance potential.

HPE’s below-peer group valuation multiple reflects the steady decline in revenues and earnings suffered across all of its businesses over the past few years. The market will likely award HPE a higher valuation, if and when its financial performance stabilizes and it begins to show signs of growth. For now, management has been able to meet its guidance each quarter, even as earnings have declined, which indicates that management is on top of the situation. Recent acquisitions offer better growth potential and management says that it has seen signs of growth in these important niche markets, which bodes well for HPE’s future. In the meantime, the stock offers an annual dividend of $0.26 per share, equivalent to a 1.5% dividend yield at the current quote. With a payout ratio of only 18%, the company should have the capacity to raise the dividend over time.

Despite the concerns about the core business, HPE management has delivered a solid total return to shareholders since splitting off from its parent company. Since its opening stock price of $18.00 on October 19, 2015. shareholders have received $0.42 in dividends and DXC shares now worth $7.16 in addition to their HPE stock, which closed at $17.18 on Friday (Aug. 18). In simple terms (without accounting for the time value of money), that works out to a total return of 37.6%. That compares with the S&P 500’s total return of 24.1% over the same time frame. The Seattle spin-off will probably add further to shareholder returns. Management gets an A+ for financial engineering, but its overall grade is so far incomplete.

The record date for the Seattle spin-off and the subsequent merger with MFI has been set at August 21 and the transaction is expected to close on September 1. Two-way trading in HPE (i.e. with and without the MFI share distribution) will begin in August 21. As with Everett, HPE shareholders will own 50.1% of Micro Focus. The transaction is expected to deliver $8.8 billion of value to HPE and its shareholders, including $6.3 billion of newly issued MFI American Depositary Shares (each ADS being equivalent to one regular MFI share) for HPE shareholders and $2.5 billion paid to HPE as a dividend from Seattle. By my estimates, the MFI stock is worth $3.77 per HPE share and HPE shareholders should receive roughly 0.135 ADSs for each of their HPE shares. (The final distribution rate is yet to be determined.)

August 19, 2017

Stephen P. Percoco

Lark Research, Inc.

839 Dewitt Street

Linden, New Jersey 07036

(908) 448-2246

incomebuilder@larkresearch.com

© Lark Research, Inc. All rights reserved. Reproduction without permission is prohibited.

Discover more from Lark Research

Subscribe to get the latest posts sent to your email.

By Notes and Analysis from HPE's Analyst Meeting - Lark Research October 27, 2017 - 7:41 PM

[…] My previous article on HPE is available here: HPE’s Transformation Continues with the Seattle Spin-Off […]