Arch Coal, the second largest U.S. coal producer, is another casualty of the sharp decline in coal consumption. After a steady slide in its business that began in 2011 and accelerated when oil and natural gas prices plunged in 2014, the company filed for bankruptcy in January 2016.

ACI’s stock has lost 99.9% of its value since its post-financial crisis high in March 2011 and now trades at about $0.40 on OTC Markets, f/k/a the “pink sheets,” under the symbol “ACIIQ”. Arch’s unsecured bonds have suffered a similar fate. Its 7% Senior Notes due 2019 ,for example, traded at 0.45% of par value, or $4.50 per $1,000 bond face value on May 12. Thus, the common stock and unsecured bonds have suffered near total losses.

Investors in ACI’s common stock and unsecured bonds have a steep uphill climb to obtain any meaningful recovery of their losses. Only a sudden and dramatic turnaround in Arch’s business would spare the common stock from being legally wiped out through the bankruptcy process. Unsecured bondholders may get common stock and warrants in the new equity of the restructured company that could conceivably represent an attractive return from current levels; but that would still only provide them with a small partial recovery of the bonds’ par value.

Restructuring Support Agreement. Immediately preceding the Chapter 11 filing, Arch Coal entered into a Restructuring Support Agreement (RSA) with its senior bank lenders. This type of agreement, which has become quite common in bankruptcies, outlines key provisions of the bankruptcy plan agreed by the company and the bank group. It is meant to facilitate a quick resolution to the bankruptcy process and is the basis upon which the banks, which clearly have the power in bankruptcy due to the seniority of their claims, promise not to take more drastic action to protect the value of their collateral. Other classes of claims and interests (such as unsecured debt and common stock) do not usually get a say in the RSA.

Arch Coal’s RSA has the following terms:

- Arch’s common stock will be cancelled.;

- The senior lenders will receive cash (estimated at $114.8 million in the company’s Disclosure Statement which was recently filed with the bankruptcy court), $326.5 million of new first lien debt and all of the equity of the reorganized company;

- Unsecured creditors, including the portions of first- and second-lien loans that exceed the estimated value of the collateral, would receive either common stock and warrants or the residual value of the company’s unencumbered assets (if any), after other priority fees, expenses and claims;

- The company’s $200 million receivables securitization facility would be reinstated or replaced; and

- Bank lenders would appoint six of seven members of ACI’s Board of Directors.

The RSA requires bankruptcy court approval. If adopted, it would reduce ACI’s outstanding debt by $4.5 billion. Senior lenders, at least 50% of whom have signed on to the RSA, would give up their claims on their $1.9 billion term loan to Arch Coal.

ACI Financial Projections. We do not yet know what value Arch Coal is assigning to its new common stock. Arch has prepared financial projections that were included in a Regulation FD 8-K filing with the SEC on April 15, 2016. In that filing, the company warns that the projections were prepared neither for public disclosure nor in compliance with SEC and AICPA standards; and their accountants did not review them. Consequently, it says that the projections should not be relied upon as a predictor of future events. Yet, the company did use them in negotiating the terms of the RSA.

Surprisingly, Arch Coal did not include those or any other financial projections in its Disclosure Statement, which was filed with the bankruptcy court on May 5. (It provided placeholders for those projections and also for its liquidation analysis in that document.) Perhaps the company needed more time to put the projections in a form suitable for the Disclosure Statement. It is also possible that its view of its future performance might have changed since the original projections were prepared.

The baseline 2015 historical performance included in the projections does not correspond exactly to the company’s audited financial statements included in its 10-K filing. The company excludes certain one-offs, like impairment charges, mine closure costs and the loss recorded on its investment in Patriot Coal. Arch’s financial projections also exclude the amortization of acquired sales contracts (a sign perhaps that it won’t utilize these going forward) and they also exclude without explanation $181 million of sales and cost of sales and $8.8 million of depreciation. (This presumably was a part of its coal business that was closed or sold during the year.)

After those adjustments, Arch’s 2015 sales were $2.39 billion and EBITDA was $250 million. The EBITDA in the projections is essentially the same as the Adjusted EBITDA reported in its 2015 10-K. From there, Arch Coal assumes that 2016 sales will decline 19.3% to $1.93 billion and EBITDA will plunge 60% to $102 million. The projections then anticipate a modest bounce back in 2017, with sales rising 4.8% to $2.03 billion and EBITDA up 38% to $141 million. In 2018, the rebound continues, but it is more gradual on the top line, with sales rising only 2.5% to $2.5 billion; but EBITDA is projected to be up another 48% to $208 million. Thus, Arch assumes that sales and EBITDA will remain below 2015 levels for the entire 2016-2018 forecast period.

Importantly, the company’s assumptions on unit sales, prices and profit margins were reduced sharply from December to March. I calculate that the company’s 2016 sales projection declined by 10.6% over that three month period and estimate that the projected cash margin on those sales declined by a comparable percentage. Much of this was undoubtedly due to the warm winter weather, but a portion was also due to a weaker outlook for met coal sales (used in steel-making). The December-March drop raises the concern that Arch’s estimates could get cut again by the time it files the financial projections with its Disclosure Statement.

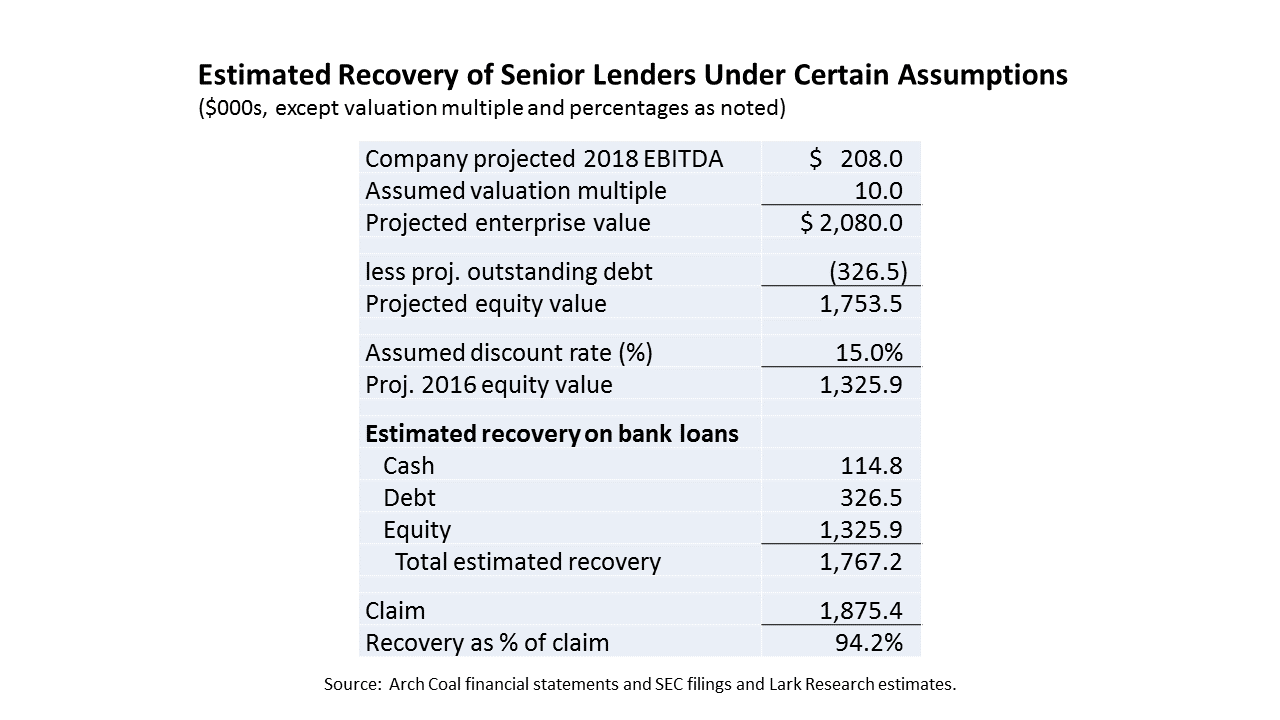

ACI Valuation. I estimate Arch’s equity value using the April 15 projections, even though they might be revised at a later date. With projected 2018 EBITDA of $208 and an assumed valuation multiple of 10, Arch’s enterprise value would be $2.08 billion, not including a projected $575 million in available cash and, I presume, about $100 million of restricted cash. Under the RSA, the bank lenders would therefore get an enterprise worth $2.08 billion plus $675 million of cash in 2018.

That $675 million cash projection does not account for the $114.8 million cash payment that the lenders would receive presumably sometime in 2016 under the RSA. It also does not include expenses associated with the bankruptcy process. Furthermore, the company requires a certain amount of cash to run the business: To keep things simple, I am going to assume that all $675 million is necessary to run the business, pay the senior lenders under the RSA and cover the costs of the bankruptcy.

Under these assumptions, I estimate that the lenders’ proposed 100% equity stake is worth $1.32 billion today. This is calculated by taking the projected enterprise value of $2.08 billion minus the $326.5 million in senior notes and discounting the net $1.75 billion at a 15% annualized rate over two years.

Total consideration to the senior lenders is therefore estimated to be $1.77 billion, which is equal to the $114.8 million cash payment, plus the $326.5 million in debt, plus the estimated present value of equity of $1.33 billion. With a total claim of $1.9 billion, their recovery would be about 94 cents on the dollar.

Of course, the lenders might say that the EBITDA valuation multiple should be lower or the discount rate should be higher. My simplified analysis also does not take into consideration the portion of the restructured equity that would be given to management. All of these would reduce the value of their proposed recovery below my estimate of 94 cents and increase the degree to which their claim is impaired.

The Risks and Opportunities of Holding Out for a Better Deal. Based upon this set of projections, I believe that the unsecured creditors probably acted correctly by rejecting the company’s initial offer of common stock and warrants. In my view, the numbers suggest that they should try to hold out for a better recovery.

With the bonds currently trading at less than a penny, there appears to be little risk of holding out. Stalling for time will cost unsecured creditors only if Arch’s performance deteriorates even more, which could result in a fire sale of the company or liquidation of its assets. In that case, the unsecured creditors will end up with nothing and will have lost the opportunity for the small recovery recently offered by the company.

It is not unusual for investors who have suffered catastrophic losses to pin their hopes on a turnaround; but the bankruptcy process typically injects a dose of reality by forcing a resolution of outstanding claims and interests so the debtor can get back on its feet as quickly as possible. With Arch, however, it is not unrealistic to think that its profitability could rebound quickly. The company projects EBITDA of only $102 million for 2016, but its adjusted EBITDA peaked at $921 million in 2011, just four-and-a-half years ago. Although there have been secular changes in Arch’s business caused by the push by the Environmental Protection Agency (EPS) to address the harmful effects of burning coal, most of the recent decline in profitability have been driven by the low price of natural gas, the strength of the dollar and unusually warm winter weather. Those factors can and indeed will reverse in time, but it is unclear whether the reversal will come quickly enough to save Arch’s unsecured creditors and equity interests.

Senior Lenders are Clearly in Charge. Over the objections of the unsecured creditors, the bankruptcy court approved the debtors’ $275 million postpetition financing agreement on February 25. That Debtor-in-Position facility was sponsored and probably will be mostly funded by Arch’s existing senior lenders. The unsecured creditors argued, among other things, that there was no cash emergency; the debtor did not need the money, the financing was too costly; and it ties up most of the debtors’ cash and thus compromises their position.

With $594 million of unrestricted cash on its balance sheet at March 31, Arch has sufficient resources to fund its operations. In its disclosure materials filed with the SEC on April 15, the company projected that it will burn through $225 million in cash in 2016 and end the year with $426 million of unrestricted cash. After that, its cash balance is projected to increase by $55 million in 2017 and $94 million in 2018.

The DIP financing does not give the company a greater cash cushion. In fact, it reduces the cash that Arch can use in the business. Under the agreement, if Arch borrows the $275 million, it must maintain a minimum cash level of $500 million. Thus, while unrestricted cash would increase to $869 million (as of March 31) upon the drawdown of the DIP facility, Arch would only be able to use $369 million to fund its business. Based upon Arch Coal’s estimated cash burn, its available cash will drop to an estimated $209 million by the end of 2016.

Still, it is reasonable for the senior lenders to seek to impose a minimum cash requirement. Arch’s unrestricted cash is part of their collateral. They do not want to risk losing that collateral, if the company’s financial performance deteriorates further.

Conceivably, the company might have taken an alternate approach. It might have argued that the claim of the senior lenders is protected adequately by the value of the company’s coal reserves. If the court agreed, it could have ruled that Arch could use its unrestricted cash to operate the business.

But the company would have faced an uphill battle in proving that assertion. Although Arch Coal’s Powder River Basin (PRB) operations have been consistently profitable over the past five years, it would be difficult to prove that they would provide enough value (i.e. generate enough cash flow) on a standalone basis to protect the senior lenders claims, including interest. Arch’s PRB’s operations, according to my calculations and estimates, do not generate enough cash flow (after estimated standalone corporate costs and capital expenditures) to amortize the senior lenders’ $1.9 billion term loan at the minimum 6.25% interest rate over the 12 year remaining life of the reserves. This is true using both the five year average and 2015 standalone results. In my opinion, the company would need to extend its PRB reserve life beyond 12 years to cover the term loan in full, but I do not know whether this is possible and if so, what the cost would be.

Arch might be able to provide enough value by throwing in the Leer mine, which was completed in 2013 at a cost of more than $400 million. However, the company’s projections suggest that the market for Appalachian metallurgical coal will be weaker in 2016, so it would probably not have been easy to seal the deal with both the senior lenders and the court on this alternative adequate protection package.

A Walter Energy Repeat? The recent outcome of the Walter Energy case raises another warning flag for ACI’s unsecured creditors. Walter’s bank lenders petitioned the court to purchase the core operations of the company in a Section 363 sale (after a stalking horse auction whereby other potential buyers were invited to top the lenders’ bid). General Motors also utilized a Section 363 sale to sidestep prepetition liabilities and make a quick exit from bankruptcy. Thus, Walter Energy’s lenders were able to “credit bid” for the core assets – i.e. acquire the core operating assets in exchange for their claims. Walter’s non-core assets were also sold to a third party.

The senior lenders were able to convince the judge that this Section 363 sale offered the best way to avoid a deterioration in the value of the company’s operations, preserve the greatest number of jobs for its employees and relieve the debtor of liabilities, including certain reclamation obligations; but unsecured creditors were left holding the bag. I don’t know what, if anything, is left in the estate after the asset sales; but probably very little, given that Walter Energy’s 8.5% Senior Notes due 2021 traded on May 11 at 0.01 or $0.10 per $1,000.00 face value.

It is worth noting that some of the professionals in the Walter Energy case – the financial advisors for the debtor (PJT Partners) and for the unsecured creditors (Berkeley Research Group) – are now in similar roles in the Arch Coal bankruptcy.

It may also be noteworthy that the Arch Coal DIP Facility similarly allows lenders to credit bid their claims (to acquire Arch Coal assets). In the Peabody Energy bankruptcy, an ad hoc group of Senior Note holders, including Aurelius Capital Management, Elliott Management, Capital Research & Management and Centerbridge Partners, objected to the inclusion of a credit bid provision in the proposed DIP Facility. The court approved Peabody’s DIP facility yesterday (5/17), but I have been unable to obtain the final order to see whether the credit bid provision was removed.

Bridging the Gap. Given the circumstances surrounding the collapse of the coal industry, there is a high risk that profitability can be as volatile on the upside as it has been on the downside. It is difficult to make the case here that the bankruptcies were brought on by mismanagement. Only a part of the industry’s recent troubles are attributable to secular trends, such as a permanent shift away from coal due to environmental concerns. Rather, most of the industry’s misfortune in recent years has been due to commodity and financial price trends (i.e. the steep drop in oil and natural gas prices and the sharp rise in the dollar). In recent months, coal demand has also fallen because of warm winter weather. Although we may not be able to predict when those price trends will reverse or when we will next experience a cold winter, it is a pretty good bet that they will at some time in the future.

For that reason, I believe that the court in the Walter Energy case failed to protect unsecured creditors (and perhaps even equity interests) from potentially handing an unjustified windfall profit to the senior lenders. Given the course of events at the outset of the Arch Coal case, I believe that unsecured creditors and equity investors face a similar risk.

One way to address the risk of windfall profits would be to utilize warrants (or similar instruments) to structure the treatment of unsecured claims in such a way as to provide them with a meaningful recovery if and when the debtor’s profitability returns. In the Arch Coal case, for example, unsecured creditors might get little or nothing until the $1.9 billion claim of the senior lenders is satisfied. Through their warrants, they might then receive the most of the appreciation in enterprise value above $1.9 billion. With better chance of a meaningful recovery in the future, unsecured creditors should be more willing to accept a bankruptcy plan that offers them little or nothing today.

The primary objection to this pattern of payouts is that it creates an overhang on the stock. Debtors might have to issue a large number of warrants to achieve an equitable distribution of recoveries. This represents significant potential dilution.

Even so, the overhang might be limited by setting a three- to five-year expiration date on the warrants or warrant-like structure. Trading in the new stock might still be affected until the warrants expire, but I believe that this would be a reasonable cost in unusual circumstances to achieve an equitable distribution in cases where unsecured creditors and equity investors would otherwise be wiped out.

May 18, 2016

Stephen P. Percoco

Lark Research, Inc.

839 Dewitt Street

Linden, New Jersey 07036

(908) 448-2246

incomebuilder@larkresearch.com

©2016 Lark Research, Inc. All rights reserved. Reproduction without permission is prohibited.

Discover more from Lark Research

Subscribe to get the latest posts sent to your email.