- GAAP loss of $1.18 billion or $0.14 per share vs. a 17Q1 loss of $0.12 billion or $0.01 per share.

- This quarter’s loss included a $1.55 billion ($0.17 per share) charge representing the estimated cost of settling potential FIRREA charges with the U.S. Dept. of Justice.

- GE’s 18Q1 adjusted industrial free cash flow was negative $1.68 billion, better than 17Q1’s negative $2.75 billion.

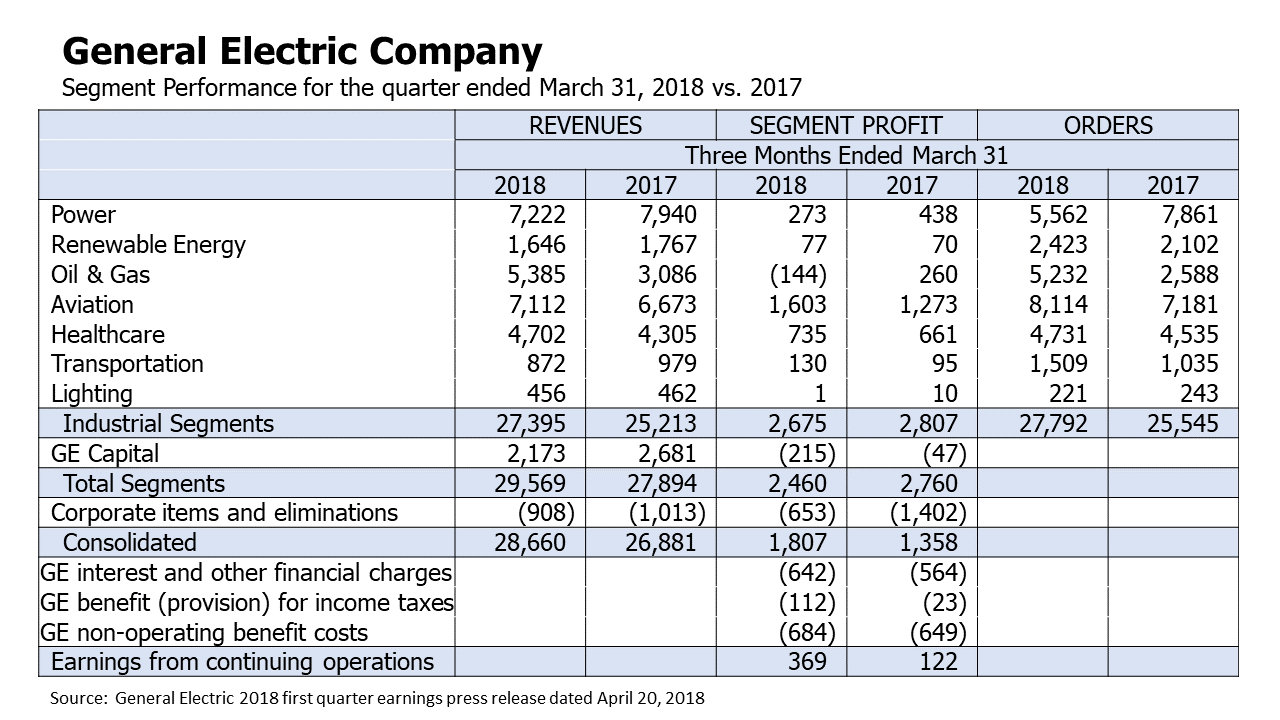

- Consolidated revenues increased 7% to $28.7 billion, due to the acquisition of Baker Hughes. Industrial organic revenues declined 4% to $23.8 billion.

- Segment profit fell 11% to $2.46 billion, due to declines at Oil & Gas, Power and GE Capital. However, after-tax earnings from continuing operations improved from $0.12 billion to $0.37 billion, due to lower corporate items and eliminations.

- CEO John Flannery said that GE made a step forward in executing on its 2018 plan, with signs of progress in its performance. The company is on track to exceed its 2018 cost reduction goal of $2 billion and is proceeding with its planned $20 billion of dispositions for 2018 and 2019.

- Under Mr. Flannery, GE may transition away from the conglomerate model toward becoming a federation of publicly-traded companies.

Industrial Segment Performance. Industrial segment revenues increased 9% to $27.4 billion, primarily due to the acquisition of BHGE. Industrial segment profit declined 5% to $2.68 billion, due to declines at Power and Oil & Gas.

I will provide some comments and observations on the performance of and issues facing GE’s Power, Oil & Gas and Aviation segments.

Power. Orders fell 29% to $5.6 billion, with declines across all of Power’s major equipment models, but service orders, excluding 2017 divestitures, rose. Based upon recent demand and expected contract closure timing, GE now sees 2018 global heavy-duty gas turbine demand of less than 30 gigawatts (GW). That compares with previous expectations of 30-34 GW. A sub-30 GW year would also be lower than the previous market bottom in 2002.

Power revenues declined 9% to $7.2 billion and segment profit fell 38% to $273 million. GE sees weakness in the business continuing through 2019. At the November Outlook meeting, management said that organic revenues would be down 10% and operating profit down 25% in 2018. First quarter results suggest that Power’s financial performance could come in below that previous guidance.

The Power team is making progress addressing current challenges. New leaders from within GE have been installed at Powers Services and Gas Power Systems, which together accounted for nearly 70% of Power’s 2017 revenues of $36 billion. Power also has a new manager of its supply chain function who reports directly to Power President and CEO Russell Stokes.

Power is downsizing operations to better align capacity with expected market demand. By closing manufacturing and repair sites and downsizing the workforce, it reduced its structural (or fixed) costs by $800 million in 2017 and has set a goal of $1 billion of structural cost out in 2018. In the 2018 first quarter, Power reported $350 million of cost out, ahead of plan.

The team is also focused on improving power’s operating efficiency and expanding its go-to-market strategy. Up until recently, Power had focused primarily on its Advanced Gas Path (AGP) upgrades that improve gas turbine efficiency, especially for GE’s F-Class turbines. The gains in efficiency from AGP upgrades help large-scale gas turbine power plants gain competitive advantage, moving them up the dispatch curve. Along with these lucrative AGP upgrades, GE often gets long-term customer service agreements (LTSAs) which help boost income, but not nearly as much cash.

While AGPs helped GE enhance and protect its franchise (especially for large scale, baseload and load-following assets), Power did not pay sufficient attention to other opportunities and challenges within the gas power market. It lost transactional business from customers who were unwilling to sign LTSAs but still needed help in addressing planned and unplanned outages. Power also apparently did not anticipate the impact of declining capacity rates on plant owners’ willingness to pursue upgrades. (Operators receive capacity payments for guaranteeing the availability of their plants to the grid on demand.) As capacity rates fell, Power was saddled with excess inventory when customers did not follow through with planned upgrades.

Power’s efforts to improve operating efficiency began with the goal of paring inventories (and improving inventory turns by 50%). It is pushing hard to reduce cost overruns and improve product delivery schedules (a task made easier in the short run by the sharp drop in equipment orders). It is also looking to cut the cost of new product introductions (in part by reducing the number of NPIs).

Likewise, Power is looking to upgrade its information systems to improve operating efficiency and reduce complexity. For example, it has already reduced the number of ERP systems deployed across its businesses by 13.5% and is well on its way toward its goal of an 80% reduction by 2020.

The reduction in capacity and improvement in operating efficiency will put Power in an even stronger competitive position. Power is also now pursuing all types of available business, contractual and transactional. Still, a meaningful rebound in its performance probably requires an upturn in industry demand.

The U.S. gas-fired electric power generation market seems saturated; but there are still growth opportunities outside the U.S. in markets where electricity is undersupplied. Power’s smaller generators are used in various applications, including marine transportation, so there will likely at least be pockets of opportunity there going forward. Given the modest diversity in end markets, it is somewhat surprising to see orders fall simultaneously across all of Power’s major product lines.

GE has previously anticipated that demand will remain weak through the end of 2019. The weaker-than-expected demand noted in the 2018 first quarter might conceivably push a recovery out further. However, demand could improve later in the year, even in the heavy-duty gas turbine market, if economic conditions remain favorable and natural gas prices remain low.

Oil & Gas. Revenues increased 74% to $5.39 billion, due primarily to the BHGE acquisition. On a combined basis, which shows prior year results as if the merger had occurred on the first day of the period, revenues increased 1%. BHGE’s short cycle businesses, which are more sensitive to near-term changes in drilling and production activity, showed revenue gains, but the long-cycle businesses, especially those serving the offshore markets, posted revenue declines.

Oil & Gas segment profit, as reported by GE, declined from $260 million to a loss of $144 million. Most of the decline was due to increases in restructuring, impairments and other charges and higher inventory impairments, which more than offset a modest decline in corporate expenses. Operating profits from BHGE’s segments were roughly flat, with improvements in Oilfield Services and Digital, offset by declines in Oilfield Equipment and Turbomachinery & Process Solutions.

BHGE continues to make progress in integrating the operations of GE Oil & Gas and Baker Hughes. It has, for example, reduced its global physical footprint by closing and consolidating facilities, including manufacturing plants. The company achieved $114 million of synergies during the 2018 first quarter and says it is on track for $700 million in synergies for the full year.

After rising from $50-$55 in late 2017, the price of a barrel of oil is now trading around $60-$70. BHGE believes that the price of oil will remain rangebound, which should give customers confidence to move forward with planned projects. BHGE thus expects that global oil & gas activity will improve steadily during the year. Although production is well off the 2016 low, it is still down significantly from the 2014 peak. Consequently, BHGE sees continued growth beyond 2018.

During the first two years of the industry downturn, it was widely reported that oilfield services companies were compelled to cut prices for many of their customers to help keep them afloat. If so, the industry should benefit proportionately more from the recovery in oil prices, recouping some of those price discounts as customer profitability recovers. This on top of the industrywide pickup in production activity should provide a meaningful boost to the financial performance of BHGE and its peers.

2018 first quarter orders increased 9% on a combined basis to $5.2 billion. All BHGE segments reported order gains. In its press release and on the conference call, management highlighted key contract wins that demonstrate BHGE competitive advantages in key product and service categories and highlight the organization’s commitment to operational excellence.

GE’s original 2018 guidance for Oil & Gas, given at its annual outlook meeting in November and reaffirmed on its 2018 first quarter conference call, anticipates a 2%-5% increase in organic revenues and 50% increase in segment profit. BHGE, as far as I can tell, has offered no specific guidance on its 2018 performance. If indeed the industry is in the early stages of a likely multi-year recovery, BHGE is positioned to continue to grow revenues and profits beyond 2018.

Aviation. Rising passenger and freight volumes continue to fuel growth in commercial aircraft orders worldwide. Aviation’s orders increased 13% to $8.1 billion in the quarter, with equipment orders up 18% and commercial engine orders (included within equipment) up 39%. Orders for the GEnx engine doubled to 24, while those for the LEAP engine jumped 52% to 994.

Aviation delivered 186 LEAP engines in the quarter, up 142% from 77 a year ago, but 70 behind plan. The lower-than-anticipated LEAP shipments held back the growth in revenues but helped boost operating margins by 80 basis points. LEAP margins during the ramping up of production are lower than those on Aviation’s mature engine models. Aviation expects to reduce the cost of the LEAP by more than 50% from its initial launch in 2015 to the end of 2018. Ramping up production is therefore key to achieving both its revenue and cost goals for the LEAP and for Aviation as a whole. Aviation expects to make up most of the missed production target during the balance of 2018, delivering 1,100-1,200 LEAP engines for the full year, up from 459 in 2017 and on its way to 1,800-1,900 for 2019.

Military engine orders rose more than three-fold from 72 to 251 in the quarter. GE sees good opportunities in the planned replacement of the USAF trainer and on fighters being developed by countries. It has also obtained good business from upgrading a large portion of the U.S. military helicopter fleet and is bidding on several next-generation aircraft.

Aviation’s services business will continue to experience solid growth because of recent and anticipated future engine sales. It reported spare parts sales of $25.2 million per day in the 2018 first quarter, up 16% from $21.7 million in the prior year. Many of the newer engines installed on commercial aircraft in recent years have not made their first shop visits. Many others have made only one service call so far.

Aviation reported 2018 first quarter segment profits of $1.6 billion, up 25.9%, on revenues of $7.1 billion, up 6.6%. GE expects that Aviation will deliver growth of 7%-10% in both revenues and profit in 2018.

Other Segments. GE’s other industrial segments reported results that were mostly in line with management’s expectations. In Renewables, segment profit increased 10% to $77 million primarily due to the acquisition of LM Wind, which more than offset pricing pressure in the base business. In Healthcare, revenues increased 9% to $4.7 billion and segment profit was up 11% to $735 million, as volume growth and productivity gains more than offset lower pricing and higher program investments. In Transportation, revenues declined 11% to $872 million because of lower locomotive volume, but operating profit was up 37% to $130 million, as increased profits from services and higher mining wheel motor shipments more than offset the decline in locomotives. In Lighting (including Current), which is expected to be sold by the end of the year, revenues declined 1% to $456 million, but segment profit fell to $1 million from $10 million.

GE Capital. GE’s Financial Services business reported a loss attributable to GE of $215 million from continuing operations in the quarter. $45 million of the loss was due to a further adjustment on the impact of tax reform on energy-related investments and $50 million reflected the cost of calling $2 billion of excess debt. Excluding these unusual items, GE Capital’s first quarter loss from continuing operations was $120 million, more than last year’s loss of $47 million.

Revenues from services declined 19% or by $508 million to $2.14 billion, due mostly to lower gains on asset sales. This was only partially offset by declines in SG&A expenses and Other costs and expenses (including restructuring charges). As a result, GE Capital’s pre-tax loss from continuing operations widened from $139 million to $321 million ($271 million, excluding the $50 million upfront costs associated with calling the debt).

Discontinued operations posted a loss of $1.55 billion, up from a loss of $242 million in 2017. During the quarter, GE Capital took a $1.5 billion charge, representing its estimate of the cost of a potential settlement with the U.S. Dept. of Justice over a potential charge that GE Capital and its former subsidiary WMC violated FIRREA through WMC’s origination and sale of subprime mortgage loans in 2006 and 2007. The estimate reflects recent discussions that GE has had with the Dept. of Justice and GE’s analysis of similar settlements reached between the DOJ and other major financial institutions.

Capital ended the quarter with $146.0 billion of assets, down from $156.7 billion at the end of 2017. On the asset side, cash declined by $7.7 billion. On the liabilities side, debt declined by $8.9 billion and equity by $1.5 billion. Virtually all the decline in shareowners’ equity was due to the FIRREA-related settlement charge.

Capital ended the quarter with $55 billion of cash (including restricted cash) and marketable securities and $22 billion of liquidity. It has sufficient liquidity now and going forward to handle the estimated cost of settling the FIRREA charge as well as the additional $12 billion in statutory capital contributions ($2 billion per year from 2019 to 2024) committed for its legacy insurance obligations.

GE Capital expects that its performance in the second half will improve because of lower excess debt costs, tax planning benefits and asset sales gains associated with the GE Capital exit plan. Continuing operations will likely be about breakeven for the year.

According to my analysis (with the limited disclosure provided by GE), it is difficult to see how GE Capital will generate sustained profitability over the next few years. Management says that GE Capital will operate near breakeven, with net profits or losses determined by future gains or losses on asset sales.

GE is committed to improving GE Capital’s capital position by the end of 2019. It continues to explore ways to rebuild equity, including through gains on incremental asset sales. It currently expects to sell $15 billion of assets over the next two years and is scaling down its presence in Energy Financial Services and Industrial Finance.

Although GE Capital’s equity base looks a bit thin with $12 billion of book equity against $146 billion of assets at March 31, it had $39.8 billion of intercompany debt payable to GE as of December 31, 2017. Intercompany debt declined by $3.9 billion in the quarter. GE could conceivably convert part of the remaining intercompany debt into GE Capital equity, if necessary.

Alternatively, GE Capital could attract a significant minority investment from a major investor or financial institution. It might also decide to pay a large insurer or investor to take away the remaining legacy insurance obligations, which would by cheered by GE investors.

Non-GAAP Metrics. At this time, I offer the following observations on and adjustments to GE’s use of non-GAAP metrics:

- I do not exclude restructuring and other charges from my assessment of non-GAAP earnings.

- I believe that GE’s exclusion of non-operating benefit costs in its determination of adjusted EPS would normally be considered inappropriate. However, management has determined that it is appropriate because it intends to eliminate these costs over the next three years by contributing $6 billion to its pension fund in 2018. Even so, I do not exclude non-operating benefit costs from my non-GAAP adjusted earnings figure.

- I do exclude the $1.5 billion recorded reserve related to the WMC FIRREA investigation, which was recorded in discontinued operations, from my assessment of non-GAAP adjusted earnings and EPS. Although I believe that this cost should be included in an assessment of GE’s long-term historical financial performance, it is a large charge that is unlikely to be repeated going forward.

With these three considerations, I estimate 2018 first quarter non-GAAP adjusted income of $316 million or $0.03 per share for GE. That compares with the prior year’s non-GAAP adjusted earnings of $121 million or $0.01 per share.

Dispositions. GE has set a target of $20 billion of asset sales in 2018 and 2019. CEO John Flannery said that the company made good progress in the quarter toward that goal. GE expects to complete the sale of the Industrial Solutions business in the second quarter (with expected cash proceeds of $1.9 billion) and Healthcare’s Value-Based Care business in the third quarter (with expected cash proceeds of $1.0 billion). It is also working to sell several small niche businesses from within Aviation, its Current and Lighting businesses, Distributed Power and its Transportation business.

The Wall St. Journal reported in April that GE would most likely opt for a partial spin-off of Transportation; but comments from management on the 18Q1 conference call left me with the impression that an outright sale is still a possibility.

GE’s Transportation business has averaged $1.07 billion in operating profit and about $1.2 billion in EBITDA over the past three years. Given its declining profitability – with operating profit of $0.8 billion and just under $1.0 billion in estimated EBITDA in 2017 – I believe Transportation’s maximum valuation would be $15 billion in a partial spin-off. If 20% of Transportation was sold in an IPO, GE would then realize up to $3 billion in proceeds before deal expenses including taxes.

An outright sale might be achievable only at a lower valuation. A financial buyer would probably have to put in a substantial amount of equity (because Transportation’s ability to borrow on a stand-alone basis is probably limited), so a financial buyer’s willingness to bid up the purchase price would be limited. But GE could provide bridge financing in the form of subordinated debt and/or take back a minority equity stake that would raise the sale price. There are probably only a few potential strategic buyers.

If GE intends to proceed with the sale, I would prefer to see a partial spin-off, primarily because I think that the business fits well with GE’s business model. (Transportation has a leading market position producing big ticket, complex machinery with lots of digital content and significant associated services). But a partial spin-off would only bring in a few billion dollars, making it more difficult for GE to achieve its stated goal of $20 billion in asset sales (unless the $20 billion includes the expected sale of $15 billion of GE Capital assets over the next two years).

Restructuring. GE’s (pre-tax) restructuring and other charges increased from $1.7 billion in 2015 to $3.6 billion in 2016 to $5.3 billion in 2017. 2017 restructuring costs included a $1.2 billion goodwill impairment charge attributable to GE’s Power business.

Cash restructuring costs have also increased, but at a more moderate pace. GE’s cash restructuring and other charges have risen from $1.0 billion in 2015 to $1.7 billion in 2016 and then to $2.0 billion in 2017.

Consolidated pre-tax restructuring and other charges for the 2018 first quarter were $522 million. Although GE’s restructuring and other charges could approach $2.0 billion in 2018, they will likely be down significantly from 2017 and should continue to decline in 2019 and beyond, barring any material adverse changes in the global economy or significant shifts in GE’s corporate strategy.

GE excludes (after-tax) restructuring costs in its determination of Non-GAAP adjusted earnings and EPS. This is useful information because it provides some perspective on what GE’s GAAP earnings may be in the future, when the company no longer incurs any of these charges. Since GE has recorded annual restructuring charges in excess of $1.5 billion since 2013, however, I do not exclude these costs in my definition of adjusted earnings and EPS for GE.

Structural Costs. GE reported that it had achieved a reduction of $805 million in industrial structural costs in the quarter, compared with the prior year. It says that it is on target to exceed its goal of $2 billion in structural costs out in 2018, but year-over-year comparisons will get tougher as the year progresses.

GE is diligent in its use of unconventional (and non-GAAP) terms. For example, it reconciles “structural costs” to the relevant GAAP metric in its quarterly supplemental data. This allows investors and analysts to track GE’s progress in reducing structural costs each quarter.

What exactly are industrial structural costs? From GE’s perspective, they are roughly equivalent to fixed costs. To calculate them, GE starts with total industrial segment costs (a GAAP metric) and subtracts out variable costs. It then subtracts “unusual costs”, such as restructuring and other charges booked during the period, structural costs attributable to business acquisitions and divestitures and related foreign exchange effects. In the 2018 first quarter, GE began adding back corporate profit (excluding corporate restructuring costs and certain gains and losses) in this calculation, so they would now be more precisely characterized as “net” industrial structural costs.

Tracking the progress on industrial structural costs was more difficult this quarter because GE changed its calculation methodology. One change was probably due to the adoption of the new accounting standard for non-operating pension costs. Under the new standard, these costs are reported as a separate line item, so GE did not have to pull them out of total industrial costs as it did before.

GE also made other changes to previously reported 2017 first quarter results, most if not all of which were due to the adoption of new accounting standards and a switch from LIFO to FIFO accounting on a significant portion of inventories. Industrial structural costs for the 2017 first quarter were originally reported to be $6.0 and are now reported at $6.5 billion.

While precise measurements are often helpful, it is important to remember that industrial structural cost is only one determinant of profitability and there are tradeoffs. GE will probably incur higher variable costs to maintain lower structural costs. For example, GE Power will likely require higher variable costs to service customers from 17 recently closed sites. It presumably made the decision to close those sites because they were not generating sufficient revenues to justify their structural costs.

Segment variable costs as a percent of industrial segment revenues increased by 130 basis points from 67.2% in the 2017 first quarter to 68.5% in the 2018 first quarter. Although the increase was probably due mostly to the acquisition of Baker Hughes and perhaps to changes in product mix, some portion of the increase might have been due to the reduction in structural costs. Despite the rise in variable costs, a quick pick-up in sales could trigger a proportionately greater increase in profits.

Given the diversity of its operations, GE will continue to make decisions about expanding or reducing capacity within each of its business segments over time. In its 2017 annual report, the company said that it will continue to monitor the economic environment and may undertake further restructuring actions to more closely align its cost structure with its earnings and cost reduction goals.

While GE has undoubtedly been eliminating some wasteful spending, its pursuit of lower structural costs also represents a reduction in manufacturing and servicing capacity. Some part of the reduction in capacity may be made possible by efficiency gains related to its digital initiatives; but the bulk of the structural cost cuts also reflects the company’s assessment of future business prospects, both with respect to the global economic outlook and to its forecasts in each industry. Industry demand in some segments, like Power and Transportation, may be saturated in the near- to medium-term. GE is presumably establishing the structural cost base that it sees as appropriate for the medium-term.

The Transformation of GE. According to CEO John Flannery, a major goal of the restructuring initiatives is to increase the primacy of the business segments while reducing the scope of corporate. Going forward, corporate will consist mostly of strategy, governance, capital allocation (i.e. finance) and talent (i.e. human resources) functions. GE will continue to leverage the horizontal capabilities of its global research and digital organizations. Lean principles will also be applied to GE’s “tier 1” business segments (e.g. Power, Aviation and Healthcare), which should result in additional cost savings.

In addition, Mr. Flannery reported that GE continues to consider the best structure (or structures) for the company and its businesses going forward. According to Mr. Flannery, the optimal structure for each business segment will facilitate an appropriate level of operating rigor, the alignment of management’s performance with the business’s goals and operating flexibility. This will help each business maximize its value to key stakeholders: customers, employees and investors.

GE is presumably looking at a range of alternative financial structures, including tracking stocks, partial or complete spin-offs or some combination of these, including a possible break-up of the company. From an investor’s point of view, I believe that Baker Hughes is a good model, because it provides a vehicle by which BHGE can increase its operating scale and grow its business, while giving investors a more complete picture of its financial and operating performance. If so, GE may decide to evolve into a confederation of publicly-traded companies, with a lean corporate headquarters and shared R&D and digital services. That structure may, however, limit the parent’s financial flexibility since it will have to consider the rights of minority shareholders in any distributions and investments of capital.

The Board of Directors is heavily engaged in this analysis, including the process by which GE might make any proposed transition. Mr. Flannery suggested that some announcements might be made in this regard by the end of the second quarter.

May 9, 2018

Stephen P. Percoco

Lark Research

839 Dewitt Street

Linden, New Jersey 07036

(908) 448-2246

admin@larkresearch.com

© 2018 by Lark Research. All rights reserved. Reproduction without permission is prohibited.

Discover more from Lark Research

Subscribe to get the latest posts sent to your email.