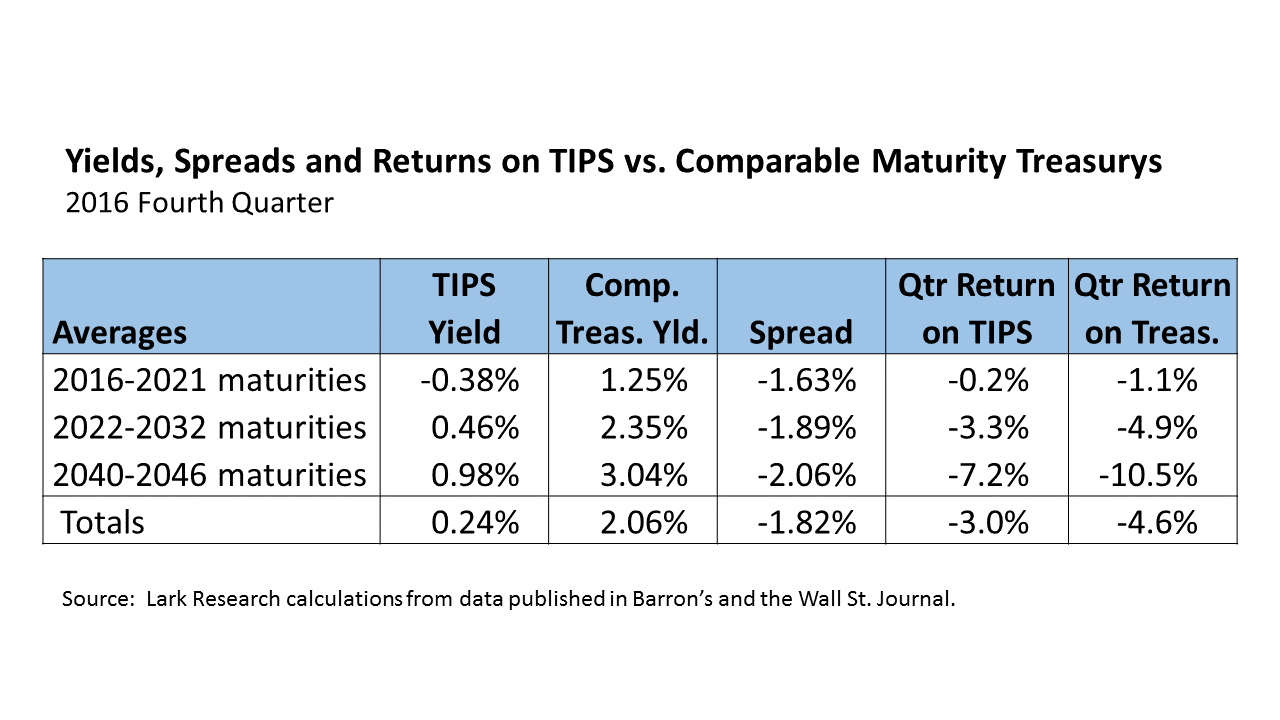

As a result of the post-election sell-off in bonds, treasury inflation-protected securities recorded a loss of 3.0% in the 2016 fourth quarter, their worst performance since the 2013 second quarter. TIPS performance slipped with each passing quarter in 2016. Perhaps the only consolation was that TIPS outperformed comparable maturity straight Treasurys, which suffered a loss of 4.6% in the quarter.

The TIPS yield curve shifted up sharply across intermediate- and long-term maturities in the fourth quarter. Yields on short-term maturity TIPS (i.e. those maturing from 2017 to 2021) were also up, but the yields on the shortest maturities (to 2018) were either unchanged or lower. The average increase in intermediate and long-term TIPS yields was about 40 basis points. Average yields (across all maturities) were positive (at 0.24%) for the first time this year. Despite the sharp increase, however, average yields ended 2016 nearly 40 basis points below 2015 year-end levels.

2016 Fourth Quarter Returns. From the 2016 third to fourth quarters, the average TIPS yield (across all maturities) increased from -0.13% to 0.24%. The average price declined by 3.7% in the fourth quarter, but this was partially offset by a 50 basis point gain due to the inflation-adjustment (equal to the increase in the CPI). As a result, the total return on TIPS was negative at -3.0%. (The numbers do not add perfectly for several reasons, including my use of averages.) Losses were greater in the longer maturities for both TIPS and comparable maturity Treasurys.

Average yields on those comparable maturity Treasurys increased by 67 basis points from 1.39% in the 2016 third quarter to 2.06% in the fourth quarter. The associated price declines more than offset coupon income. The average straight Treasury security posted a total return of -4.6%. Long maturity Treasurys suffered losses averaging 10.5%.

The yield spread between TIPS and straight Treasurys increased by 30 basis points during the quarter to -1.82%, still well within recent historical norms. The current spread reflects expectations that inflation will remain below 2% for the foreseeable future. Investors who believe that CPI inflation will be lower would earn higher returns by holding comparable maturity straight Treasurys.

TIPS vs. Treasurys: Annual Returns for 2016. Despite the negative returns for the fourth quarter, the average TIPS posted a return of 4.4% in 2016. Gains earlier in the year, especially in the strong first quarter (as investors flocked to bonds to escape the plunging stock market) more than offset the fourth quarter losses. TIPS also outperformed comparable maturity straight Treasury securities, which earned 1.2% for the year. This was the first year that TIPS outperformed straight Treasurys since 2012.

Outlook. With the economic gaining momentum, TIPS could face further headwinds in 2017, if the interest rate normalization process continues. In the near-term, however, the rise in yields has been steep; so interest rates could fall back before heading higher. The rise in oil prices should spark a modest pick-up in inflation, which raises the odds that TIPS will outperform Treasurys again in 2017.

January 6, 2017

Stephen P. Percoco

Lark Research

16 W. Elizabeth Avenue, Suite 4

Linden, New Jersey 07036

(908) 975-0250

admin@larkresearch.com

© 2017. Lark Research, Inc. All rights reserved. Reproduction without permission is prohibited.